How Moving Up the Capital Stack Can Reduce Your Investment Risk

By Paul Moore

Never miss an Invest Clearly Insights article

Subscribe to our newsletter today

Preferred Equity: How Moving Up the Capital Stack Can Reduce Your Investment Risk

Do you remember what Warren Buffett did at the worst moment of the 2008 Financial Crisis?

You may think he waited until everything hit rock bottom. After all, who wants to catch a falling knife?

Or maybe you think he stopped investing altogether… especially in financial stocks, which looked about as appealing as juggling chainsaws.

Nope. Wrong on both counts.

At the height of the worst financial crisis since the Great Depression, Buffett invested $5 billion in Goldman Sachs.

It was September of 2008. Bear Stearns was history. Lehman Brothers had collapsed. Observers, regulators, and internal staff speculated that Goldman Sachs could be next. Goldman’s stock had already fallen by roughly two-thirds, and some thought it was headed to zero.

So why on earth would Buffett step in?

There were several reasons. But one matters most for real estate investors.

Buffett didn’t buy common stock.

He invested in preferred equity.

Berkshire Hathaway’s $5 billion preferred equity investment:

- Was shielded from first loss position by common and GP equity

- Paid a guaranteed 10% annual dividend

- Provided meaningful upside if Goldman recovered

Goldman did recover. And between 2008 and 2011, Berkshire earned approximately $3.7 billion in dividends, premiums, and warrant profits on its original $5 billion investment.

That’s not bravery. That’s structure.

What Can Real Estate Investors Learn from This?

Quite a lot.

After a short stint as a multifamily syndicator, my firm began offering funds. Along with professional due diligence, these funds provided diversification across asset types, operators, geographies, and strategies.

As large LPs, we often negotiated better terms. But structurally, we were still LPs. No control rights, no remedies, no legal ability to look under the hood. And like all LPs, we sat squarely in first-loss position.

That worked just fine for several years. The tide was rising, and as Buffett famously warned, rising tides make everyone look like a good swimmer.

Then the tide went out.

Beginning in the spring of 2022, eleven interest rate hikes changed the landscape almost overnight. High-flying syndicators were suddenly pausing distributions, doing capital calls, and even losing deals back to lenders. And years later, much of this is still playing out.

We were already conservative by nature, but now our process was being tested.

Was there a way to meaningfully reduce downside risk without abandoning real estate… or settling for bond-like returns?

That question led us to one of the most important pivots we’ve made.

We changed positions in the capital stack.

By structuring investments as preferred equity, we created a materially larger margin of safety.

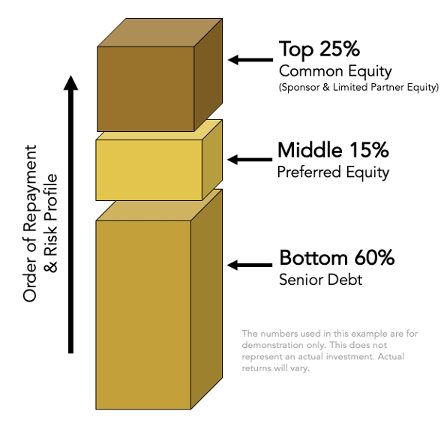

How Does Preferred Equity Change the Risk Profile?

Preferred equity sits between debt and equity in the capital stack. Preferred equity…

- Shares advantages (and downsides) of debt and equity

- Has payment priority ahead of common equity

- Lowers downside risk exposure than common equity

- Has no lien, but more upside and tax benefits than debt

- Is a compelling risk-return ratio

Preferred equity utilizes common equity as a shield against loss. Preferred equity’s last dollar risk is significantly less than common equity held by LP investors.

In a deal where preferred equity’s last dollar of risk sits at 75% loan-to-value, common equity absorbs all losses above that threshold. Common equity’s risk begins at 100% LTV.

If the property value declines by up to 25% in this example, common equity bears the entire loss. Preferred equity principal remains intact.

That’s margin of safety in action.

Preferred equity also typically receives fixed payments along the way (similar to debt). And unlike LP equity, preferred investors can negotiate real rights and remedies:

- Budget approvals

- Management oversight

- Control provisions

- The right to force a sale if the deal is going off the rails

Layer those protections on top of a fundamentally sound asset and competent management, and you’ve added multiple lines of defense.

In my previous post, we discussed why investors should stop chasing the highest ROI and instead pursue the best risk-adjusted ROI.

This is a textbook example.

What Does Private CRE Preferred Equity Invest In?

To be clear, this has nothing to do with the “preferred return” commonly referenced in syndications. This is a separate investment class, negotiated independently between investors and operators.

Preferred equity is typically utilized in situations like these:

- Value-Add Acquisitions. Preferred equity can fill a gap in the capital stack. Syndicators with clear deal upside accept the higher coupon to close the deal, often planning to refinance the preferred equity out later.

- Recapitalizations. Many operators locked in long-term, low-rate debt between 2018 and 2021. After creating significant value, they may want to access equity without triggering prepayment penalties or refinancing into higher rates.

- Development Deals. Developers frequently use preferred equity on top of construction debt. It’s also used when projects run over budget or beyond original timelines.

- Rescue Capital. Some operators use preferred equity to avoid foreclosure when suffering from escalating floating-rate debt, rising expenses, or soft rents strain cash flow.

A brief word of caution: rescue capital deserves careful scrutiny. Sometimes it saves a deal. Sometimes it’s simply throwing good money after bad. Discernment matters.

A Preferred Equity Case Study

About a year ago, a $16 million preferred equity investment recapitalized a workforce multifamily portfolio in Illinois. Sponsor selection was top priority.

This syndicator launched in 2012 and owns and operates over 2,500 workforce units concentrated in a single region. The firm is vertically integrated with in-house property and construction management, creating efficiencies and economies of scale.

Track record is imperative. This sponsor completed 59 full-cycle investments (1,327 units) with a 26.2% IRR.

The recapitalized portfolio included 67 properties (1,034 units) acquired between 2018 and 2020. Investors receive depreciation pari-passu with common equity.

The loan portfolio consists of 10 loans with an $89 million balance. Nine of ten loans mature between 2031 and 2053. Significant value had already been created, and the operator wanted access to some of it without refinancing.

Key negotiated terms included:

- Current pay senior to all other equity distributions after debt service

- Full return of capital and accrued upside before common equity receives capital event distributions

- Forced sale rights in the event of imminent lender foreclosure

- Approval over capital expense budgets

- Investment not subject to any operator-level fees and splits

The structure provided a 10% current pay plus 6% accruing and compounding upside, payable at a liquidity event. There was a 1.35x minimum equity multiple if the preferred equity was repaid early.

Individual investors expect up to 8% current yield and a 14% to 15% total annual ROI. The projected equity multiple over a three-to-five-year hold is 1.42x to 1.75x.

No one expects to double their money.

No one expects fireworks.

But given the downside protection, contractual income, and rights LP investors never receive, many may prefer this investment over a development deal targeting a 30% IRR

I certainly did.

How Can Individuals Invest in Preferred Equity?

These opportunities aren’t easy to find… and not all deliver superior risk-adjusted returns. But here are three common paths:

- Invest in a preferred equity fund or deal. These managers specialize in structuring preferred equity investments and typically bring deep due diligence, underwriting expertise, and active asset management.

- Invest directly in a syndicator’s fund or deal. Some sponsors raise preferred equity to bridge shortfalls or complete business plans. These deals require careful scrutiny, particularly when used as rescue capital.

- Create your own preferred equity investment. Family offices and ultra-high-net-worth investors sometimes negotiate preferred equity directly. This route involves extensive underwriting, inspections, legal work, and meaningful upfront costs, but can be well worth it for the right partner/deal.

Final Thoughts

Investment risk isn’t eliminated by optimism, spreadsheets, or clever marketing decks.

It’s managed by structure.

Two investors can invest in the same property, with the same operator, in the same market… and experience radically different outcomes… simply because they occupy different capital stack positions.

Common equity can produce extraordinary returns in favorable environments. But as the last few years have reminded us, it also absorbs the first losses when markets turn.

Preferred equity offers a different tradeoff: less upside in exchange for materially better downside protection, contractual cash flow, and control when things go wrong.

That tradeoff won’t appeal to everyone. And it shouldn’t. But for investors focused on capital preservation, steady compounding, and the possibility of superior risk-adjusted returns over full cycles (not just bull markets) changing position in the capital stack deserves serious consideration.

Buffett didn’t abandon discipline in 2008. He doubled down on it… by insisting on structure, priority, and margin of safety.

Real estate investors would be wise to do the same.

Written by

Paul Moore is the Founder of Wellings Capital. After graduating with an engineering degree and an MBA, Paul entered the management development track at Ford Motor Co. He later scaled and sold a staffing firm to a public co. in 1997. Paul began investing in real estate in 1999 to protect and grow his own wealth. He completed over 100 real estate investments, appeared on HGTV’s House Hunters, and developed a subdivision. After completing three commercial developments, Paul narrowed his focus to commercial real estate in 2011. Paul is married with four children and lives in Central Virginia. Press: Paul was 2x Finalist for Ernst & Young’s Michigan Entrepreneur and has contributed to BiggerPockets and Fox Business. He is the author of two real estate books: The Perfect Investment and Storing Up Profits. Paul co-hosted a wealth-building podcast called How to Lose Money and he’s been a featured guest on 300+ other podcasts including the BiggerPockets Podcast, The Real Estate Guys, and Entrepreneur on Fire.

Read Our ReviewsOther Articles

What Every Good Deck Should Have When Evaluating Real Estate Syndications

What makes a good investment deck? You do not need a marketing masterpiece. You need transparent data that helps you answer the question, “Do I want to invest the time to learn more?

The Pause & Pivot: What the Fed’s Rate Means for Your Real Estate Syndications

The economy is still running too hot for the Fed to comfortably keep slashing rates. After a brief sigh of relief with three consecutive rate cuts at the end of last year, the Federal Reserve hit the brakes in January, holding the benchmark rate steady at 3.50% to 3.75%. So what does this mean for investors?

Why Investor Voices Matter More Than Ever

Industry analysts have described a “data transparency crisis” in private markets, citing fragmented reporting, inconsistent data standards, and limited comparability across managers. This matters because limited visibility affects how investors assess sponsors, price risk, and respond when execution diverges from expectations.

Why “Better Structure” Beats “Higher Returns” Over Full Market Cycles

If you are tired of acting as the shock absorber in the common equity first-loss position, Paul Moore argues it is time to rethink where you sit in the capital stack, introducing the engineered downside protection of JV Hybrid Equity.

Limited Partners in Private Real Estate and Private Investments

If you’re exploring private real estate investing, you’ve likely encountered the term “limited partner” or “LP.” Understanding this role is essential before committing capital to any private market fund

Investor Experience Index: 2025 Wrap Up

We’ve analyzed review data from 2025 to uncover surprising trends in private real estate.